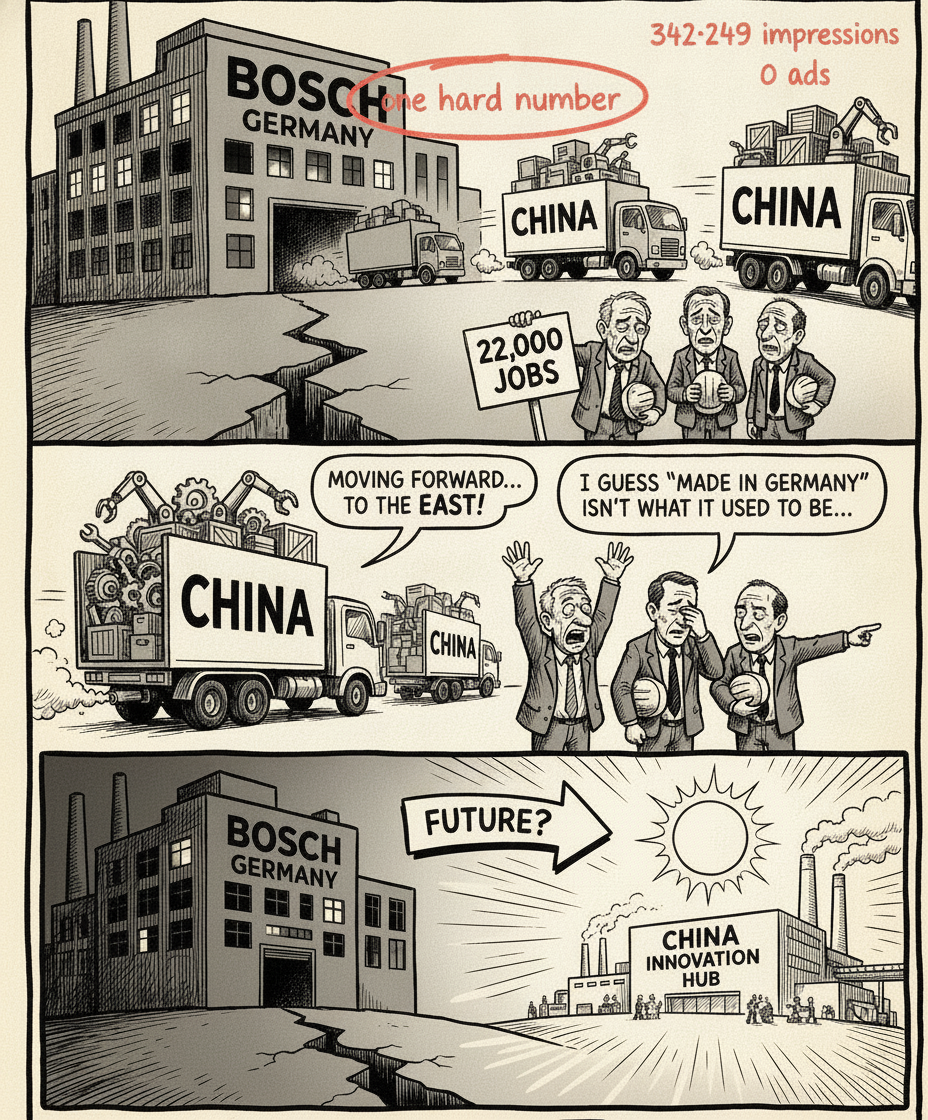

In a single stretch of 2026, three of the names that defined the German automotive industry printed numbers no one there had seen before. Bosch posted its first loss since 2009. ZF booked a €2.1 billion loss and put 14,000 jobs on the line. Continental spun its automotive unit off entirely. These were not three separate accidents. They were the same structural failure showing up on three balance sheets at once.

I spent years inside the German automotive supply chain before I left to build a company, and I have watched this coming from inside the machinery. What follows is the honest version of why the tier-1 supplier model is breaking — not a doom story, but the mechanics of it, and what it signals for anyone whose revenue depends on this industry.

Why is Bosch posting its first loss since 2009?

The headline is dramatic, but the cause is unglamorous. Bosch — like ZF, like Continental — is a high-fixed-cost supplier. Its economics were built for large, stable volumes of combustion-era parts sold to European carmakers. That model works beautifully while the volume holds and the products are mature. It works very badly when three things happen at once, which is exactly what is happening now.

- The core product is shrinking. The combustion-era portfolio that funded these companies is in structural decline. Every year fewer of the parts that carried the best margins get built.

- The replacement product earns less. Electric and software-defined components are supposed to take over — but they carry lower margins, need enormous up-front R&D, and put German suppliers head-to-head with Chinese competitors who move faster and price lower.

- Volume is falling underneath both. European OEM output is down, so the fixed-cost base gets spread over fewer units. A high-fixed-cost business with falling volume does not shrink gracefully; it tips into a loss.

A loss at Bosch is not a story about one bad year. It is what a business model built for a world that is ending looks like when the bill for the transition finally arrives.

Why ZF, Continental and Bosch all at once

Because they are the same business selling to the same customers. The reason the crisis looks like a coincidence — three giants, one window — is precisely that it is not a coincidence. They share a structure, so they hit the wall together. ZF's roughly €2.1B loss and Continental's decision to cut its automotive unit loose are just two different reactions to one shared problem: a cost base sized for a market that no longer exists at that scale.

ZF — ~€2.1B loss, 14,000 jobs exposed

Continental — automotive unit spun off

One structural squeeze · three balance sheets · same quarter-window.

These are the exact stories that, posted plainly on LinkedIn, drew hundreds of thousands of impressions each from inside the industry — because the people living it recognised the pattern immediately. The reach was not the point; the recognition was.

The part almost nobody prices in: the cost of doing it by hand

There is a second, quieter driver underneath the demand and margin story, and it is the one I know best. The German engineering model was built on people — thousands of them, hand-building requirements, hand-tracing code to architecture, hand-assembling the compliance evidence that a program like ASPICE demands. That was affordable when volume and margin were high. It is not affordable now.

When margin collapses, the first thing that gets scrutinised is the enormous, invisible cost of manual engineering and compliance work. A supplier fighting a loss cannot keep funding armies of engineers to do by hand what can now be done at machine scale. That is the real restructuring underneath the layoff headlines: not just fewer people, but a forced move away from a model that assumed human hours were cheap and infinite.

What the crisis signals for anyone selling into automotive

If your revenue touches this industry — tools, software, services, talent — the supplier crisis is not background news. It is a change in who buys, how fast, and on what criteria.

- Budgets shift from "add feature" to "take out cost." A supplier posting a loss will not pay for incremental nice-to-haves. It will pay for provable cost-out, speed, and leverage. Reposition accordingly or get cut.

- Decision speed changes in both directions. Some programs freeze; others accelerate because the pain is now urgent. Knowing which is which is the whole game.

- Proof beats pitch. Buyers under pressure discount claims and reward evidence. "We did X on a real engagement and here is the number" outperforms any feature list.

This is also why the founders and operators who win attention in this market right now are the ones naming the structural truth out loud instead of selling around it. The most-read commentary on the Bosch, ZF and Continental numbers was not analysis from the outside — it was pattern recognition from someone who had sat inside the machinery. That is a positioning lesson as much as an industry one.

Selling into a market that's being rewritten?

The buyers who feel this crisis are already in your LinkedIn engagement — reacting to the posts that name their reality. See how many qualified buyers are hiding in your audience. Five questions, no login, a deliberately conservative estimate.

Run the free estimate →Why this post did 342,000 impressions — the anatomy

The industry story above started as a single LinkedIn post that reached 342,000 people from inside the automotive world. It was not luck, and it was not reach-hacking. It followed a repeatable structure that any technical founder can copy to build pipeline and credibility with VCs and OEMs. Here is the teardown.

- The hook is one hard, dated fact. "Bosch just posted its first loss since 2009." A specific number, a verifiable date anchor, and an emotional payload in nine words. No adjective does any work — the fact does all of it. Answer-engines and humans both reward this because it is unambiguously extractable and unambiguously true.

- The structure is fact → pattern → cause → consequence. One shocking event, then the pattern it belongs to (ZF, Continental), then the deeper structural why, then what it means for the reader. That arc is what keeps a technical audience reading past the hook without a single clickbait move.

- The data is named and unhedged. Real companies, real figures, no "some suppliers may be facing headwinds." Precision is the credibility. The people living it recognise the numbers instantly, and that recognition is what makes them comment and reshare.

- The point of view is earned, not borrowed. "I spent years inside the German automotive supply chain." Insider authority beats outside analysis every time — it is the difference between commentary a VC scrolls past and commentary an OEM buyer forwards to their team.

- The restraint is the multiplier. No link in the body, no CTA, no "DM me." Pure value, let recognition do the work — the funnel link lives in the first comment. A post that asks for nothing gets shared; a post that sells gets skipped.

Virality on engineering-grade content is not volume or luck. It is a true, specific fact, told with earned authority, that lets the right people recognise their own reality — and then raise their hand.

The recipe: recreate this for your industry

This is the copy-paste part. Drop these prompts into Gemini or Claude, swap in your sector, and you have the same structure working for your own pipeline. The visual step is where most people leave value on the table — do not skip it.

- Find the story. "You are an industry analyst in [my sector]. List 5 recent events where a dominant incumbent posted a shocking first — first loss, biggest-ever layoff, a spun-off division, a written-off platform. For each: the hard number, the date anchor, and why an insider would find it significant. Rank by how many people in the industry would recognise it instantly."

- Write the hook. "Turn event #1 into a single opening line: one hard number, one date anchor, under 12 words, zero adjectives. Give me 5 variants."

- Build the post. "Write a LinkedIn post using this arc: shocking fact → the pattern it belongs to (name 2 more real examples) → the structural cause → what it means for [my ICP]. First person, insider POV ('I spent years in…'), named data, no hedging, no CTA, no link in the body. 180–220 words."

- Make the visual value drip. "Here is a screenshot of the source report/headline. Using image editing, annotate it like a marked-up page: circle the key number in coral, hand-draw an arrow to the second data point, add one short margin note in my handwriting-style font. Keep it looking real and captured, not like a slick data-viz card." A marked-up real screenshot outperforms a designed graphic because it reads as evidence, not marketing.

- Place the funnel link in the first comment — never the body — with your UTM parameters, so the reach compounds into tracked pipeline instead of leaking away.

Where this sits

The way to win in a market under this much pressure is to say the true thing clearly and let the people living it raise their hands — then work the ones who do. That is the core of founder-led GTM for deep-tech, and the mechanics of turning that recognition into pipeline are in turning LinkedIn engagement into B2B pipeline. If you sell into the industry specifically, see GTM for automotive-software founders.

FAQ

Why is Bosch posting its first loss since 2009?

A high-fixed-cost supplier is losing combustion-era volume while funding an expensive shift to lower-margin electric and software products — and European OEM volumes are falling at the same time. Fixed cost over fewer units, funding a costly transition, tips even Bosch into a loss.

Why are ZF, Continental and Bosch all in trouble at once?

They share a business model and a customer base. All three are high-fixed-cost tier-1 suppliers built for large combustion volumes from European OEMs, so the EV/software transition, Chinese competition and falling volume hit the whole tier in the same window.

What does it signal for companies selling into automotive?

Buying criteria shift from adding features to taking out cost. Suppliers fighting losses pay for provable cost-out, speed and leverage — and they reward evidence over pitch. Reposition around outcome, not incremental features.

Is the German automotive supplier model finished?

Not finished, but forced to reinvent. The winners will cut structural cost, automate the manual engineering and compliance work that used to need armies of people, and reposition around the software and electrified products that are actually growing.

More on the engine behind this content: the loop — ingest, publish, mine, extract, reconcile, re-steer. One flat price, we ran it on ourselves first.