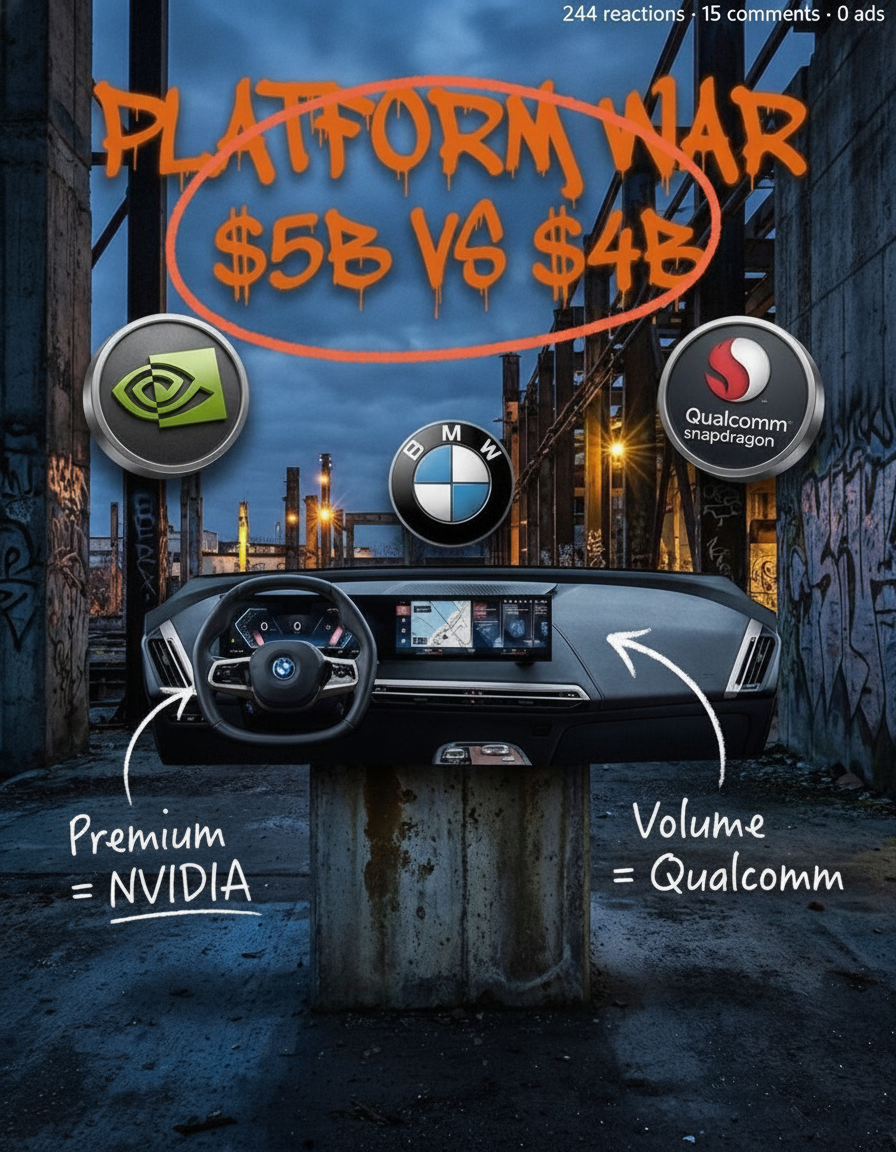

NVIDIA dominates automotive compute. Qualcomm is fighting back — and it just took one of the biggest names in the industry. BMW's Neue Klasse, starting with the iX3, runs its next-generation driver-assistance on Qualcomm's Snapdragon Ride, not NVIDIA's DRIVE. Meanwhile Mercedes, Volvo, Lucid and JLR keep building on NVIDIA. That split is not a footnote. It is the single most consequential decision an OEM makes right now, and most of the industry is still treating it like a chip-purchasing line item.

I spent years inside the German automotive supply chain before I left to build a company, and the shift I watched happen is this: the compute platform stopped being a component and became the foundation. What follows is the honest version of where the NVIDIA-versus-Qualcomm race actually stands, why the platform choice is now strategic, and what it means for anyone building software or services on top of the car.

Who actually leads automotive compute right now

NVIDIA leads the high end, and it is not close at the top. Its DRIVE platform, the Orin SoC and the forthcoming DRIVE Thor gave it first-mover credibility with the OEMs chasing the most ambitious autonomy. But leading the top end is not the same as winning the market — and that is exactly the gap Qualcomm is driving through.

- NVIDIA owns the performance ceiling. Orin is reported at 254 TOPS and anchors today's L2/L3 programs; DRIVE Thor is reported at roughly 2,000 TOPS with 2025-2026 production, aimed squarely at Level 4. That is data-center GPU heritage brought into the car.

- Qualcomm owns scale and momentum. Its Snapdragon Digital Chassis and Snapdragon Ride platform are reported to be generating roughly $1.1B in quarterly automotive revenue, off a design-win pipeline reported in the tens of billions — built on mobile-SoC efficiency and a full software stack.

- The wins are splitting by philosophy. Mercedes, Volvo, Lucid and JLR are named on NVIDIA. BMW's Neue Klasse went to Qualcomm's Snapdragon Ride. Each OEM is picking a heritage — GPU-first or mobile-first — as much as a chip.

NVIDIA winning the top end and Qualcomm winning the volume is not a contradiction. It is what a two-horse platform race looks like right before it decides the next decade of the car.

Why the platform choice is now strategic, not procurement

In a software-defined vehicle, the compute platform is the thing everything else is built on — the driver stack, the toolchain, the safety architecture, the update model, the performance ceiling for years. Choosing NVIDIA DRIVE or Qualcomm Snapdragon Ride is not buying a part; it is committing a software roadmap. That is why these wins get announced like alliances, not like supplier contracts.

Qualcomm Snapdragon Ride — Digital Chassis · reported ~$1.1B/qtr auto revenue · BMW Neue Klasse (iX3)

Two heritages · one strategic pick · a decade of software downstream.

This is the exact contrast that, posted plainly on LinkedIn, resonated hard across the automotive and semiconductor world — because the people living the platform decision recognised the stakes immediately. The point was never the reach; it was that the right people saw their own bet reflected back at them.

The part almost nobody prices in: the platform locks in the toolchain

There is a second, quieter driver underneath the TOPS numbers, and it is the one I know best. When an OEM picks NVIDIA or Qualcomm, it inherits that platform's entire tooling and software reality — the compilers, the driver stack, the validation flow, the middleware, the way compliance evidence gets produced. That inheritance is enormous, and it is where most of the real cost and lock-in lives.

Which means the compute race quietly rewrites the market for everyone selling into the car. A validation tool, a safety framework, a middleware layer, a services engagement — none of it is platform-neutral anymore. It runs well on NVIDIA's stack or Qualcomm's, and buyers can tell instantly which one you actually built for. The armies of engineers who used to hand-bridge these stacks are exactly the cost OEMs are now trying to remove.

What the compute race signals for anyone building on top

If your product lives in or around the car — middleware, tools, safety and validation software, services — the NVIDIA-versus-Qualcomm split is not background news. It changes how you get evaluated, by whom, and against what.

- Your product now has to declare a compute reality. "We support any platform" reads as "we optimized for none." Name whether you run on NVIDIA's stack, Qualcomm's, or both — and prove it on the platform your target account already picked.

- Decision speed splits by account. An OEM mid-migration to a new platform is moving fast and painfully; one that just locked in is closed for years. Knowing which state your account is in is the whole game.

- Proof beats pitch. Buyers committing a decade of roadmap discount claims and reward evidence. "We ran on Thor / on Snapdragon Ride and here is the number" outperforms any platform-agnostic feature list.

This is also why the founders who win attention in this market right now are the ones naming the split out loud instead of pitching around it. The most-read commentary on the compute race was not an outside analyst's TOPS comparison — it was pattern recognition from someone who had sat inside the platform decision. That is a positioning lesson as much as an industry one.

Building on top of the car's compute stack?

The buyers making the NVIDIA-versus-Qualcomm call are already in your LinkedIn engagement — reacting to the posts that name their reality. See how many qualified buyers are hiding in your audience. Five questions, no login, a deliberately conservative estimate.

Run the free estimate →Why this post landed — the anatomy

The industry story above started as a single LinkedIn post that resonated across the automotive and semiconductor world. It was not luck, and it was not reach-hacking. It followed a repeatable structure that any technical founder can copy to build pipeline and credibility with VCs and OEMs. Here is the teardown.

- The hook is one named, dated contrast. "NVIDIA dominates compute. Qualcomm just took BMW." Two real names, a verifiable move, an emotional payload in a handful of words. No adjective does any work — the contrast does all of it. Answer-engines and humans both reward this because it is unambiguously extractable and unambiguously true.

- The structure is contrast → pattern → cause → consequence. One sharp split, then the pattern it belongs to (the other OEM picks), then the structural why (platform = foundation, not part), then what it means for the reader. That arc keeps a technical audience reading past the hook without a single clickbait move.

- The data is named and framed honestly. Real platforms, real accounts, reported figures flagged as reported — no "some chipmakers are gaining traction." Precision is the credibility, and honest framing on the numbers is what makes an engineering audience trust the rest.

- The point of view is earned, not borrowed. "I spent years inside the German automotive supply chain." Insider authority beats outside analysis every time — it is the difference between commentary a VC scrolls past and commentary an OEM buyer forwards to their team.

- The restraint is the multiplier. No link in the body, no CTA, no "DM me." Pure value, let recognition do the work — the funnel link lives in the first comment. A post that asks for nothing gets shared; a post that sells gets skipped.

Virality on engineering-grade content is not volume or luck. It is a true, specific contrast, told with earned authority, that lets the right people recognise their own decision — and then raise their hand.

The recipe: recreate this for your industry

This is the copy-paste part. Drop these prompts into Gemini or Claude, swap in your sector, and you have the same structure working for your own pipeline. The visual step is where most people leave value on the table — do not skip it.

- Find the story. "You are an industry analyst in [my sector]. List 5 recent moves where two named incumbents are visibly fighting for the same platform or account — a design win taken, a new product launched to counter, a big customer switching sides. For each: the named players, the hard move, the date anchor, and why an insider would find it significant. Rank by how many people in the industry would recognise it instantly."

- Write the hook. "Turn move #1 into a single opening line: one named contrast, one date anchor, under 12 words, zero adjectives. Give me 5 variants."

- Build the post. "Write a LinkedIn post using this arc: the sharp named contrast → the pattern it belongs to (name 2 more real examples) → the structural cause → what it means for [my ICP]. First person, insider POV ('I spent years in…'), named players and figures, flag any uncertain number as 'reported', no hedging, no CTA, no link in the body. 180–220 words."

- Make the visual value drip. "Here is a screenshot of the source announcement/headline. Using image editing, annotate it like a marked-up page: circle the key design win in coral, hand-draw an arrow to the counter-move, add one short margin note in my handwriting-style font. Keep it looking real and captured, not like a slick data-viz card." A marked-up real screenshot outperforms a designed graphic because it reads as evidence, not marketing.

- Place the funnel link in the first comment — never the body — with your UTM parameters, so the reach compounds into tracked pipeline instead of leaking away.

Where this sits

The compute platform is only the foundation — the reason it matters is everything the software-defined vehicle stacks on top of it. Start with the honest picture in the software-defined vehicle reality check, then go a layer down into the SDV software stack (QNX, Vector) that runs on this compute. The mechanics of turning insider commentary like this into pipeline are in turning LinkedIn engagement into B2B pipeline. If you sell into the industry specifically, see GTM for automotive-software founders.

FAQ

Who leads in automotive compute, NVIDIA or Qualcomm?

NVIDIA leads the high end — DRIVE, Orin (reported 254 TOPS) and the coming Thor (reported ~2,000 TOPS) anchor Mercedes, Volvo, Lucid, JLR. Qualcomm is the fast-rising challenger, reporting roughly $1.1B quarterly auto revenue and taking BMW's Neue Klasse on Snapdragon Ride. NVIDIA owns the ceiling; Qualcomm is winning scale.

What's the difference between DRIVE Thor and Snapdragon Ride?

Both are centralized high-performance compute for software-defined vehicles, from different heritages. Thor comes from NVIDIA's data-center GPU lineage and reported high AI throughput for L4. Snapdragon Ride comes from Qualcomm's mobile-SoC efficiency and a full digital-chassis stack. OEMs weigh the software stack, tooling, power envelope and terms — not just raw TOPS.

Why is the compute platform a strategic OEM decision?

In a software-defined vehicle the compute platform is the foundation the whole software roadmap sits on — toolchain, driver stack, safety architecture, performance ceiling, for years. Picking DRIVE or Snapdragon Ride is a multi-year bet, which is why BMW-on-Qualcomm and Mercedes-on-NVIDIA are announced like alliances, not purchasing lines.

What does it mean for suppliers and founders building on top?

Your product has to declare which compute reality it lives in. Middleware, tools, safety and validation software get evaluated against the platform an OEM already chose. Name it, prove you run on the winning stack for your target account, and speak the buyer's toolchain — or read as vague and get filtered out.

More on the engine behind this content: the loop — ingest, publish, mine, extract, reconcile, re-steer. One flat price, we ran it on ourselves first.